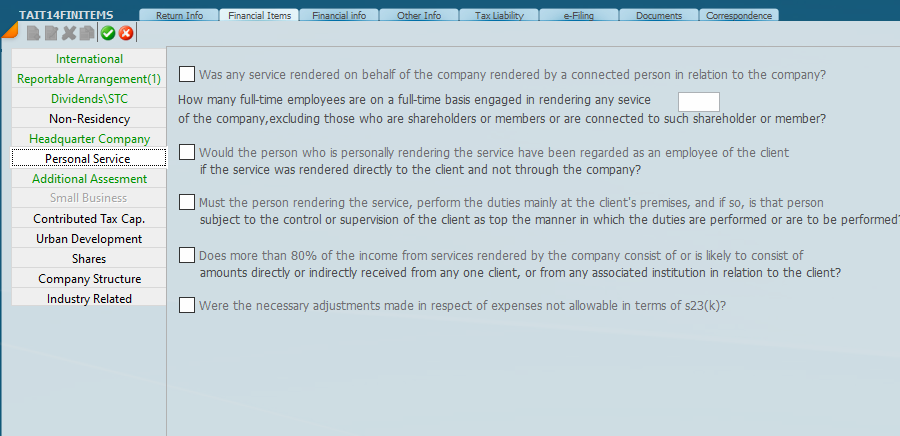

On the main screen if Personal Service is ticked this screen will be available for entry.

In South African tax law, when people refer to “personal services in a company”, they are usually referring to a Personal Service Company, which the Income Tax Act calls a “personal service provider” (PSP) (often a company/CC or trust used to supply an individual’s services to a client).

### What it means (in plain language)

A company/CC/trust is treated as a personal service provider where a connected person (typically the shareholder/member/beneficiary) personally renders the service to the client, and the arrangement looks like employment disguised through an entity.

### When a company/trust is a “personal service provider” (core tests)

A service entity is a PSP if any one of the following applies:

1) Employee test

If the individual would have been regarded as an employee of the client had the person rendered the service directly (instead of through the company/trust).

2) Control / supervision + client premises test

If the duties are performed mainly at the client’s premises and the person/entity is subject to the client’s control or supervision regarding how the work is performed.

3) 80% income test

If more than 80% of the entity’s income from services during the year is received (or likely to be received) from one client (or that client’s associated institutions).

### Key exclusion (“safe harbour”)

Even if the above tests are met, the entity will not be a PSP if it employs three or more full-time employees throughout the year who:

- are engaged in rendering that service; and

- are not shareholders/beneficiaries, and not connected persons to them.

### Why it matters (PAYE treatment)

The Fourth Schedule treats a personal service provider as an “employee” for PAYE purposes, meaning the client may have to withhold PAYE from payments made to that entity.

5 May 2026